If you’re looking for info on how to create a mobile payment app, here’s a good place to start. I’ll take you through all the steps and share the best practices around security, design, and other aspects of the p2p payment development process.

I promise you’ll walk away with enough insights to create a payment app that has a genuine potential to trump the competition.

Top Takeaways:

- By the end of 2023, more than half of smartphone users in the U.S. will transact via p2p mobile apps.

- The most promising p2p payment solutions include transactional platforms, crypto-based p2p mobile wallets, messaging-based payment apps, and standalone p2p mobile applications.

- The secret sauce to launching a successful peer-to-peer mobile payment app is an experienced agile team, prototyping, and releasing an MVP with a trackable referral program.

Table of Contents:

- P2P Payment App Market Trends

- How Do P2P Money Transfer Apps Work?

- How to Make a Peer to Peer Payment App?

- Step1: Before You Call a Mobile Payment App Development Agency

- Step 2: Design the App’s Architecture

- Step 3: Craft the App’s UI/UX

- Step 4: Behind the Scenes of P2P App Development

- Step 5: The App is Live – Now What?

- P2P Payment App Development Best Practices

- Harnessing AI and Machine Learning in P2P Payment Apps

- Challenges and Solutions in P2P Payment App Development

- Regulatory Updates: Navigating the Legal Landscape of P2P Payment Apps

- Cost of Developing a P2P Payment App

- Topflight’s Experience with p2p Payment Apps

- How Topflight Can Help

P2P Payment App Market Trends

As you probably know, “p2p” in “p2p payment app” stands for peer-to-peer or person-to-person, which means we use such apps to transact with people we know.

To create a p2p payment app that stands out in today’s diverse marketplace – where traditional mobile banking apps, standalone p2p payment apps, payment platforms, and crypto payment applications coexist – it’s crucial to understand the latest trends and features. One of these trends is the shift towards p2b (peer-to-business) transactions, which is a significant evolution from the original p2p model.

This development opens up new opportunities for businesses and consumers alike by allowing business payment options, but also presents unique challenges in terms of security and user experience. That’s definitely one of the trends with payment apps, and we’ll discuss it below, but first, let’s look at the different types of p2p payment apps that exist today:

- traditional mobile banking apps

- standalone p2p payment apps

- payment platforms

- crypto payment applications

For a deeper dive into creating your own crypto token, we recommend checking out our detailed guide.

Traditional mobile banking apps

Whether you use Wells Fargo, Chase Mobile, or any other mobile application from a bank or credit union, they all have an option to send money to your friends and family members. Some call these p2p apps “bank-centric,” but they are just bank-owned.

The p2p payment feature per se is but an option in these mobile banking apps, and it’s often not very handy, especially if people you transact with bank in a different institution. Keep reading to find out creative ways to supercharge your p2p payments, even if it’s nestled within a larger banking app.

Related: Mobile Banking App Development Guide

Standalone p2p payment apps

Services like a Cash App and Venmo focus specifically on payments and act as digital wallets, often come with a debit card and/or connect to an existing bank account. Put simply, these services exist to offer users more flexibility with managing their money.

They may have different perks, but the main premise is to let us transact effortlessly with people we trust, using built-in e-wallets. We can add existing bank accounts or create new ones, etc.

You can find more info on how to make a mobile wallet app in a separate blog.

Payment platforms

Zelle is the most prominent player in this niche. While the product exists as a mobile app (in fact, overly simplistic), Zelle is much more than mobile software for real-time payments.

First and foremost, Zelle is a platform with a robust back end and APIs that allows for interbank electronic money transfers between individuals right from within their online banking apps. Essentially, Zelle serves as an enterprise solution, a conduit that empowers banks to facilitate secure and effortless transactions for customers across various banking applications, thereby redefining the landscape of the fintech industry.

Crypto payment applications

Any crypto wallet app is already a p2p payment application allowing people to send and receive crypto as cross-border transactions. Still, you’ll need to spend a lot of time trying to find a p2p payment app for crypto as elegant and straightforward as, say, Venmo or PayPal. Other examples include Rabby Wallet and Trust Wallet.

There’s a lot to handle because different crypto tokens and coins have unique addresses, and you still need to handle payments via QR codes or type in long strings of symbols (without 100% recipient verification) to send funds.

We discussed how to develop a crypto wallet app in a dedicated blog.

Messaging apps with built-in payments

This financial sector is dominated by Facebook Pay, which works in all company’s products and requires existing banking products to transact with friends, run a fundraising campaign, or donate to creators.

The key differentiation here is that payments are tightly integrated with a chat. By the way, the only way for p2p payments in Apple Pay is also via messaging.

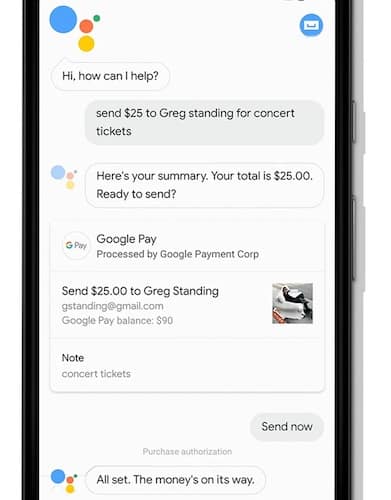

Google/Samsung/etc. Pay

I consider Apple, Google, Samsung, Android Pay, and similar payment services a stripped-down version of traditional banking apps. They do have the p2p payment functionality, but like with banking apps, it’s just another option, and the core features and benefits are for retail shopping.

People love P2P payments

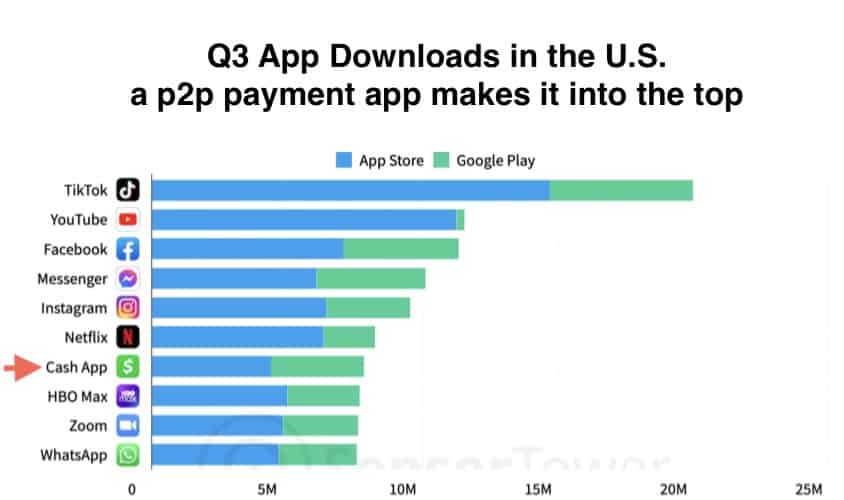

COVID-19 certainly played its role in popularizing p2p mobile payment systems. When cash changing hands is frowned upon for being inconvenient and risky for health, digital transactions become the only viable alternative.

I don’t want to overburden you with statistics, but here are a few key facts proving that p2p payment app development is a very lucrative direction:

- Valued at a hefty $4.83 billion globally in 2023, the p2p payment market is forecasted to adjust to a still robust $3.07 billion by 2028. A shift, indeed, but could this be indicative of a maturing and stabilizing market? Especially, given all the sactions at play today, flying left and right.

- With 62% of U.S. smartphone users, that’s 148.8 million people, currently using P2P mobile payment apps, the sector is set to expand even further. Projections show over 180 million users by 2026, indicating a booming market.

- Fraud is also escalating, with total losses hitting an alarming $1.7 billion in 2022, a 90% increase from 2021. Furthermore, 8% of all banking customers report falling victim to a p2p scam within the last year.

Trends in p2p payment applications

Modern mobile p2p payment solutions continue to branch out with more features, opening up new use cases and simplifying digital cash flows. Here are some trends to inspire you as you build a money transfer app:

- payments built into chats and social networking applications (social transactions)

- voice interfaces to transfer money (Siri, Alexa, Google Assistant)

- contactless payment methods (QR, NFC, Bluetooth)

- payments to sellers (besides the trusted circle of people)

- options for cashing in checks remotely

- branded credit cards

- rewards and bonuses

- cross-border crypto peer-to-peer payments

- basic crypto trading

- crypto payment platforms

- minimal or zero transfer fees

- currency exchange rates

- showing investment profits and losses

2023 and beyond trends include:

- growing use of AI to fight fraud

- biometric authentication to improve security

- instant loans (“buy now pay later”)

- FedNow for insta-payments (now live for banks and credit unions)

- lurking Central bank digital currencies (CBDC)

- NFC stickers for contactless payments on phones that don’t have NFC chips

- integrations with wearables (RFID/NFC)

- social e-commerce (including donations)

- peer-to-peer fundraising and crowdfunding

- integraitons with PoS platforms

- integrations with budgeting services and banking-as-a-service providers

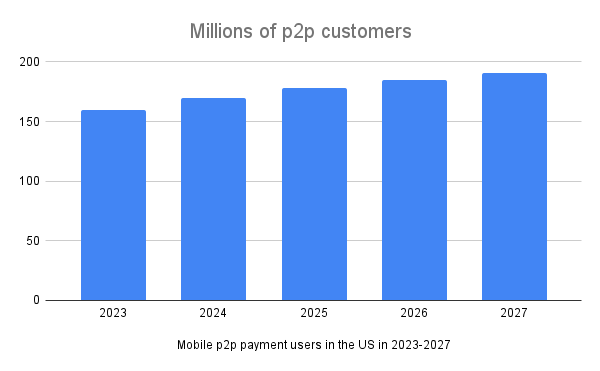

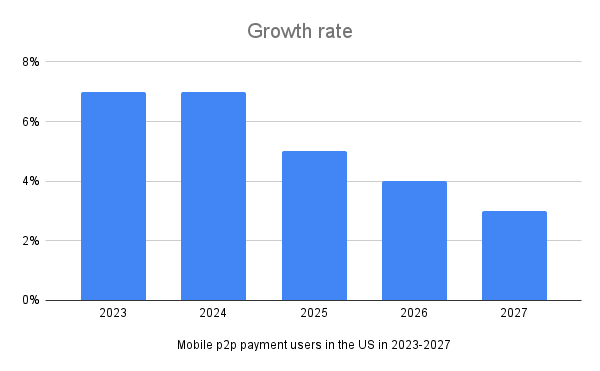

Also, take a look at US Mobile P2P Payments Forecast 2023 by Insider Intelligence: the user base is growing, but the growth rate is stalling. So, innovating becomes vital.

If you want my opinion, I envision innovations coming from banks starting to accept crypto payments and partnering with startups that offer novel ways for exchanging digital cash between people. Another growth area is adding trading options and family savings accounts.

If you want my opinion, I envision innovations coming from banks starting to accept crypto payments and partnering with startups that offer novel ways for exchanging digital cash between people. Another growth area is adding trading options and family savings accounts.

![]()

Here’s a crazy idea for a crypto-based p2p payment app. A customer sends a payment to her friend. The p2p payment service she uses converts her funds into crypto and performs AI-assisted arbitrage trading on crypto exchanges, increasing the initial transaction value. The company then splits the profit with the receiver of the initial payment. In the end, the customer’s friend receives 5-10% more than the original amount sent. That would make payments last a little longer, but imagine the game theories you could employ here. Users could agree on how long they are willing to wait for the payment to arrive, and the interest would increase proportionally to the wait time. Anyways, just an idea for online payment transfer app development.

How Do P2P Money Transfer Apps Work?

P2p money transfer apps have revolutionized the way we handle our finances, making transactions quick, easy, and convenient. But how exactly do these apps work? Here’s a brief overview:

- User Registration: This is the first step in using a p2p payment app. Users are required to create an account by providing their personal information. This often includes their name, email address, and phone number.

- Bank Account Linking: For transactions to occur, users need to link their bank accounts or credit cards to the app. This allows for seamless transactions between the app and their bank accounts.

- Contact Addition: Users can add contacts within the app for easy money transfers. They can search for other users by their registered email address or phone number.

- Transaction Initiation: To send money, users simply enter the amount they wish to send and select the recipient from their contact list.

- Security Checks: To ensure the security of transactions, P2P payment apps use various measures like two-factor authentication and encryption.

- Transaction Confirmation: Once a transaction is completed, users receive a notification confirming the transaction.

- Balance Management: The app provides features that allow users to check their balance, view transaction history, and manage their funds.

- Fund Withdrawal and Deposit: Users can withdraw money from their app accounts to their linked bank accounts or deposit money from their bank accounts into the app.

How to Make a Peer to Peer Payment App?

Creating a P2P payment app involves several steps, each crucial to ensure the app’s functionality and success. Here’s a quick step-by-step overview before we dive deeper:

- Step #1: Define Your Business Model. Understand who your target audience is, how you will monetize your app, and what makes your app unique in the market. Familiarize yourself with the legal and regulatory landscape of p2p payment apps in your target market. And secure key partnerships with financial institutions or payment processors to facilitate transactions within your app.

- Step #2: Design the App’s Architecture. Determine the key components of your app and choose the right tech stack for your app’s backend and frontend.

- Step #3: Craft the App’s UX/UI. Develop a prototype and gather user feedback to ensure your app is user-friendly and intuitive. Then work on polishing the graphical assets.

- Step #4: Develop the App. Assemble a team of developers, QA engineers, and project managers to build and test the app’s code using Agile.

- Step #5: Implement Security Measures. Incorporate strong security features like encryption and authentication to protect user data and transactions.

- Step #6: Launch and Monitor. Release your app and continuously monitor user feedback and app performance to make necessary improvements.

Step 1: Before You Call a Mobile Payment App Development Agency

Before you actually begin to build a p2p payment app, there’s a lot of things you need to clear up. It all starts with defining your strategy.

1.1: Strategize around your business model

Before you create a p2p payment app, it’s crucial to identify the exact needs of your target audience; in other words, you need market research: study your target audience and find out about their unique needs and the context for using your solution. That will help you refine your unique selling proposition and zero in on the perfect product-market fit.

- Who will use your app?

Do you create an app for money transfers for families, millennials, senior people, or an entirely niche group like stay-at-home moms and dads? Is your app going to be international or local? The more demographic characteristics you have, the deeper should be the analysis of the needs of your target market.

- When and in what context will users refer to your product?

On-the-go is just one scenario, and you can certainly go deeper, e.g., by reviewing what situations urge people to use the app, how often, etc. Will they use the app for on-the-spot, face-to-face transactions?

- How will you monetize your solution?

Many startups often put off discussing their monetization options. However, it’s strongly advised to know how your app will make money from day one.

Related: App Monetization Guide: Tips, Tricks and Best Practices

This research will naturally cover studying your competition. You’ll find a lot of helpful info on trusted software review sites, in app-store reviews, etc.

Obviously, to start a money transfer app generating real traction, you need to come up with some novel use cases. Otherwise, it will be hard to steer new customers away from already established market players.

Obviously, to start a money transfer app generating real traction, you need to come up with some novel use cases. Otherwise, it will be hard to steer new customers away from already established market players.

![]() Let’s say we want to build a shared cash pool for friends where each member can borrow once a month in turn. The longer you don’t borrow and the more you’ve contributed to the pool, the bigger loan you can claim when your turn comes. At the same time, the pool keeps generating a monthly interest distributed among all participants. The bottom line is think of an exciting killer feature (currency exchange?) to make a peer-to-peer payment app that really stands out.

Let’s say we want to build a shared cash pool for friends where each member can borrow once a month in turn. The longer you don’t borrow and the more you’ve contributed to the pool, the bigger loan you can claim when your turn comes. At the same time, the pool keeps generating a monthly interest distributed among all participants. The bottom line is think of an exciting killer feature (currency exchange?) to make a peer-to-peer payment app that really stands out.

1.2: Research regulatory requirements

Of course, we can come up with ideas like I mentioned nonstop. However, the feasibility of your solution will largely depend on regulations. Cross-border money transfer apps face the most significant challenges simply because they need to comply with regulations in every single geography where they plan to operate.

Therefore, it’s best to start with the U.S., and more specifically, with particular states. Make sure your development partners are comfortable working with PCI DSS (the Payment Card Industry Data Security Standard).

1.3: Secure key partnerships

Let’s face it: you can’t make an app like Venmo without securing a partnership with a credible financial institution that supports bank payments.

Every major neo banking app emerged backed by a traditional bank, and many continue to run along these rails.

Every major neo banking app emerged backed by a traditional bank, and many continue to run along these rails.

Related: How to build a neobank app

So evaluate your options and seek key partnerships that will secure the core payment app features.

1.4: Choose a development partner

Once you’ve identified your app’s product-market fit, reviewed legislation barriers, and discussed it with potential partners, it’s time to hail software developers.

What team composition do you need to develop a money transfer app? Well, it will take some talent:

- UX/UI designers

- Full-stack developers for creating the server-side

- Mobile developers to build apps for smartphones

- QA engineers to sift out errors

- Project manager to coordinate the whole team

- Product manager to keep the end goal aligned and collaborate on your product’s vision

A battle-tested team versed in fintech app development services will help you polish your lean canvas, taking into account the technological and business challenges of the envisioned product.

We love to kick off projects at Topflight with what we call a collaborative pre-flight workshop. We help you craft a lean canvas, prioritized list of features aligned with ROI expectations, and strategic roadmap during the workshop.

Step 2: Design the App’s Architecture

In practice, the next two steps I will describe happen side by side, simultaneously. So there’s absolutely nothing stopping you from defining the app’s architecture and simultaneously designing its user experience.

2.1 Who orchestrates the p2p payment app’s architecture?

That’s possible because “architecture” in this case means identifying the main building blocks of the solution and choosing the most appropriate tech stack for this structure. You will need someone of a CTO (chief technical officer) caliber, backed by lead mobile developers for this task. As for the design phase, which is taking place simultaneously, we’ll discuss that in the next step.

- architecture and design can happen simultaneously

- you need a CTO and lead developers for the task

2.2 How does that really work?

It’s like when you build a Lego castle with your kid; you pick bigger parts to lay down the foundation. Same with software architecture, only instead of bricks you choose programming languages, frameworks, databases, APIs, cloud services — in a nutshell, everything that breathes life into your solution.

Considering you have chosen a qualified development team to create a p2p payment app, it will help you make the right decisions about your app’s architecture:

Considering you have chosen a qualified development team to create a p2p payment app, it will help you make the right decisions about your app’s architecture:

- your app for money transfer should scale easily

- the platform should feature top-notch security

- ideally, the software should easily integrate with other financial services

What are the primary building blocks that make up the architecture of a p2p payment app? Well, there are quite a few. On a high level, depending on the intended app functionality, you’d have to look at:

- p2p payment protocol (for payment processing)

- multiple databases (for the apps and internal monitoring and other services)

- risk assessment module (AML, anti-fraud)

- authentication service (plus KYC)

- mobile and web user front ends

- multiple internal and external APIs; API gateways

- app performance monitoring

- a logging instance

This list may sound a little intimidating to a business owner, especially when they discuss it with software architects in detail. However, at a very high level, it’s just apps that customers and employees work with, databases, and many tools to interconnect the data with user interfaces and analyze it.

2.3 Questions to bounce off your p2p payment app developers?

Ultimately, the tech stack and architecture specifics will depend on your developers’ strengths and expertise. At the same time, they develop a payment app according to your vision. So you kind of guide them (with the right team, it’s a collaborative process) through this process, asking questions that matter most to end-users and the platform owner.

- How many transactions should we be able to process per second out the gate?

- How many users does it take to bring the system to a screeching halt?

- How quickly can we scale up?

- How many layers of protection do we need to set up to secure the software?

- How do we ensure our app can integrate with this or that service to introduce new exciting features later down the road?

Simple questions like these lead to fundamental decisions about your p2p payment software structure.

2.4 Friendly advice

What tech stack is best? As you probably know, many startups have to pivot during development or shortly after releasing an MVP. So a word of advice here is not to lock yourself into technologies you won’t be able to change later unless you’re 100% sure about your roadmap.

Related: MVP App Development: Best Practices, Steps, Tools

- opt for an open-ended tech stack that will last minimum for a decade

- refrain from brand-new technologies not providing enough edge over competitors

Another suggestion is to think outside the mobile platforms. For example, voice assistants work across many devices, not just smartphones. You may want to create a single API to connect with Siri, Google Assistant, and Alexa.

You can find more advice on how to build a fintech app in a separate blog.

As you define your app’s architecture and simultaneously design its user experience, have you considered what it takes to make a p2p payment app that not only functions seamlessly but also delivers an exceptional user experience? Remember, in the crowded fintech space, it’s not just about creating another standard app – it’s about crafting a unique platform that meets user needs while offering them a simple, intuitive, and efficient way to handle their financial transactions.

Step 3: Craft the App’s UX/UI

The next stage is rapid prototyping. The idea is to create an interactive graphical shell of your app that anyone can click through and understand how it works. Note that the UX/UI creation can happen simultaneously with scoping architecture.

3.1 Who does rapid prototyping?

At this point, you mainly engage with UX/UI experts who visualize your concept, adjusting it to the target audience’s tastes and needs. However, developers’ input is also required. They assess what features are feasible on a given mobile platform and help find the most appropriate approach to honor Apple’s and Google’s interface guidelines.

- designers

- mobile developers

3.2 How do you run prototyping?

You’d then use this prototype with test users matching your demographics to see how they interact with the software. As a result, you get insights that you can use to rehash the prototype and verify that it’s easy to use and effectively addresses users’ needs.

In other words, users need to move between screens seamlessly and be fully aware of what’s going on and what to expect.

- gather feedback from test users

- iterate on the prototype to achieve the ideal ease of use

Once you’ve cemented the user-friendly UI/UX of the app, designers will need to mark up all graphical assets and make them ready for developers, i.e., design hand-off kicks in.

Related: UI/UX design guidelines to build a successful app

3.3 Why do you need prototyping at all?

Here’s the big WHY you need to start with a prototype. Fleshing out the graphical shell of an application and connecting all screens together via “hot points” is nowhere near as costly as coding the actual app. Plus, prototyping takes considerably less time than coding.

- prototyping is less expensive than coding

- helps cement the product-market fit

So, when considering how to make a peer to peer payment app remember that starting with a prototype is a strategic move. It’s not only cost-effective but also allows you to visualize the user journey and ensure that your app truly fits the market needs. After all, isn’t it smarter to identify potential roadblocks or enhancements during the prototyping phase rather than post-coding?

Step 4: Behind the Scenes of P2P App Development

At this point, you should have:

- Lean canvas

- Polished design

- Well-researched architecture blueprint

You are now well-positioned to start money transfer app development. Instead of lamenting how business owners often find this step boring, let me tell you what it looks like from the inside.

4.1 Who makes a peer-to-peer payment app?

This phase is when developers fully move into the spotlight. Mobile developers make a payment app in Android and iOS, full-stack engineers code the back end with databases, APIs, and front end developers build browser-based money transfer portals for customers and admins (with user management modules).

Developers are soon joined by QA engineers, who help them set up a testing environment and look for any visual and functional glitches in the software. This collaboration ensures you make a peer to peer money transfer app that’s bug-free and optimal at performance.

To coordinate everybody’s efforts, there must be a project manager, who tracks the team’s performance on a daily basis. And there’s also a product manager who makes sure that whatever is being developed remains aligned with the business owner’s vision.

- mobile/full-stack developers

- test engineers

- product/project manager

That’s the min team composition required to create a p2p money transfer app.

4.2 How does agile p2p payment software development work?

Full disclosure: we are an agile shop. So if you engage a development agency on a fixed-price basis, the scenario will be different.

With agile, the process is pretty straightforward. The team creates a backlog of all tasks, plans two-week sprints, and executes on the selected tasks while also analyzing their performance during past sprints.

Project managers ensure you get full access to our internal processes to always be aware of what is being worked on. As we move from sprint to sprint, you start getting early versions of the apps and documentation, which guarantees the project longevity.

Once we have a stable market-ready version of the software, we can release it to the public. The deployment process usually takes at least a week because we need to deploy web apps to a production environment, upload applications to app stores, and test all functionality once again.

A couple of things you need to know about agile specifics:

- your vision may change later down the road based on the market reaction to MVP versions

- accordingly, designers may need to step in to provide UX/UI enhancements

- the agile cycle for successful projects (build > test > release) never really ends, only slowing down or intensifying instead

- the maximum and minimum hourly effort (based on involved resources) may fluctuate throughout the project

Related: Agile App Development: How to build a winning app

This agile approach allows us to bypass a slow and often misguided specification phase, cuts time-to-market, maximizes the role of your customers in shaping your p2p payment app, and overall ensures smooth and efficient delivery.

Considering the complexities and nuances that come with the decision to build a p2p payment app, our agile approach offers a balance of speed, flexibility, and customer-focused development. This method allows for continuous refinement and adaptation, which is critical in a rapidly evolving fintech market. So, whether it’s responding to user feedback or integrating new features, our agile process ensures that your app remains competitive and relevant, meeting the needs of your customers effectively.

Step 5: The App is Live – Now What?

Typically, business owners don’t think much post releasing a product when they create a money transfer app. Funny thing, the party only breaks up once you release your p2p payment application.

First of all, you will definitely spot opportunities for improving your app based on user feedback. That may have to do with altering user flows a little or introducing new features (e.g., adding a borrowing request option, etc.).

Second of all, Apple and Google will at some point release new mobile OS versions introducing new options that your software can make use of.

Put simply, development work never stops for successful products. Developers, designers, and testers keep churning new versions behind-the-scenes. Some mobile experts would argue that update frequency is one of the critical metrics for an app’s success.

So, you’re ready to create a p2p app? Remember, launching the app is just the beginning. The real journey starts when users begin to interact with your product. It’s a continuous process of learning, refining, and upgrading to meet evolving user needs and technological advancements. After all, isn’t it true that the most successful apps are those that keep growing and improving over time?

P2P Payment App Development Best Practices

I bet you feel like many details get left behind, like a list of specific technologies or advice on building an admin portal. The thing is, this stuff varies wildly from project to project. Along the same vein, I won’t pretend I know all the features your app should have. In fact, it’s something we collaborate on during the pre-flight workshop.

At the same time, we need to mention quite a few things to make sure you get the most of whatever team you work with. So, where should you direct your attention when you create an online payment app?

Security

For any software dealing with money, data protection is a crucial aspect. Users should feel safe and protected at all times, trusting your solution with their hard-earned money.

Frankly, it would take another blog to describe all the security facets you need to foresee in a p2p payment app. Let’s touch on the areas you absolutely can’t miss:

- employ machine learning and AI for automatic risk assessment

- use only trusted third-party SDKs/APIs and limit them to secondary features

- rely on strong data encryption for transferring money and financial data

- use on-device biometric authentication options for secure authentication

- enable two factor authentication with one time passwords (OTP)

- hide credit card details (like a card number, personal data, etc.)

- employ role-based access control for the admin web portal (unique IDs, OTP)

- keep an audit trail, logging all actions and transaction history on the platform

- implement session time limits

- monitor the internet connection and block the money transfer application if a user’s IP suddenly changes

As a matter of fact, it makes sense to maintain a standalone security center that monitors all activity in your p2p payment software — on the customer and business sides.

Open architecture

Remember that the more integration capabilities your software has, the quicker you’ll be able to respond to the market by integrating with new services.

That also works in the opposite direction. Suppose other companies can build add-on products connected to your p2p payment platform. In that case, you may soon discover yourself in a thriving ecosystem.

UX/UI flexibility

Personalization is still king when it comes to user interfaces. Customers love being able to adjust what they see on their screens. If you slap on that some AI, slightly augmenting their experience by surfacing the most frequently used options — you’re golden.

Voice and messaging interfaces

If you can wire, say, your utility payment right now with a simple voice command, consider yourself lucky. Even though voice interfaces are finding their place on more and more devices, many users still don’t have the p2p option to make and receive payments, or the experience is too puzzling.

Having a chatbot to help customers around your app is another good idea.

Also Read: How to Build a Messaging Application

Continuous improvement

If you include app analytics during the development step, you can catch invaluable data on app usage later on and use it for further product development. In-app analytics is also a great way to measure your app performance and monitor bugs.

Also read: Gamification in Banking: Process, Design, Best Practices

So , if you’re still wondering how to develop a p2p payment app keep in mind that it’s about building a secure, user-friendly platform that continuously adapts and improves based on user feedback and market trends. It’s a journey that involves meticulous planning, strategic execution, and a relentless commitment to enhancing user experience. Ultimately, the success of your app hinges on your ability to integrate robust security measures, offer an open architecture for easy integrations, provide a personalized UI/UX, incorporate voice and messaging interfaces, and commit to continuous improvement based on in-app analytics.

Harnessing AI and Machine Learning in P2P Payment Apps

Have you ever wondered how these peer-to-peer payment applications manage to keep your transactions secure, or how they seem to know what you want before you do? The answer lies in artificial intelligence (AI) and machine learning (ML). These advanced technologies are reshaping the p2p payments landscape, enhancing everything from security to personalization. Let’s take a closer look at how:

- Fraud Detection: Imagine an app that could spot a scam before you even knew it was happening. Machine learning algorithms, like those offered by Sift, can detect unusual behavior patterns that may indicate fraudulent activities, enhancing security for all users.

- Risk Assessment: Ever been turned down for a loan and not known why? AI platforms like Zest.ai can analyze vast amounts of data to assess the creditworthiness of users, enabling more accurate and fair lending decisions.

- Personalized User Experience: Who doesn’t love a personal touch? By analyzing user behavior and transaction history, AI services like BankBuddy can provide personalized recommendations, making each interaction feel tailored just for the user.

- Chatbots and Virtual Assistants: Need help right now? AI-powered chatbots, like those powered by Microsoft Azure Bot Service or ChatGPT, can provide immediate responses to user inquiries, improving customer satisfaction and reducing response times.

- Predictive Analysis: What if you could see into the future? Machine learning services like Google Cloud’s AutoML Tables can analyze past data to predict future transactions, helping users plan their finances.

- Automated Transactions: Tired of forgetting to pay your bills? AI services like Stripe can automate routine payments, ensuring bills are paid on time without any user intervention.

But as exciting as these AI features sound, implementing them is no walk in the park. Developing AI capabilities from scratch requires a significant investment of time, resources, and expertise. But don’t worry, you don’t have to reinvent the wheel. Many companies offer ready-made AI engines that can be integrated into your p2p payment app, providing you with advanced capabilities without the development headaches.

As a founder of a peer-to-peer mobile payment app, if you are in search of an AI engine to handle your specific use cases such as gamification, personalization, or chatbot integration, a simple Google search is likely to yield numerous ready-made solutions. These solutions are generally much easier to integrate into your platform than developing similar capabilities from scratch.

So, why not take advantage of these technologies to give your P2P payment app a competitive edge? With AI and ML, the possibilities are endless, and the future looks bright.

Challenges and Solutions in P2P Payment App Development

Developing a p2p payment app is no small feat. There are numerous hurdles to overcome, but don’t let that deter you. After all, where’s the fun without a little challenge? Let’s delve into some of these obstacles and explore solutions that can turn them into stepping stones towards success.

Gaining User Trust: Now, this is a big one. In a world where data breaches make headlines every other day, how do you convince users to trust your app with their hard-earned money? Well, the answer lies in being transparent. Make your data handling processes crystal clear. Keep your privacy policies user-friendly and easy to understand. And remember, nothing builds trust like good customer service. Consider AI-powered chatbots for instant and efficient support.

Achieving Regulatory Compliance: Ever feel like you’re lost in a maze of regulations? You’re not alone. Achieving regulatory compliance can be a daunting task, especially when you’re operating globally. Staying up-to-date with both global and local regulations is half the battle. Consult with legal experts regularly. Also, consider compliance-as-a-service providers, like ComplyAdvantage, to make your journey smoother.

Scalability: Think your app is ready for prime time? Not so fast! Can it handle a sudden surge in users? Building your app on a scalable cloud infrastructure and using a microservices architecture allows for easy scaling and updating, ensuring your app can cope with growth and change.

Interoperability with Other Financial Systems: Not all who wander are lost, but your users might feel that way if they can’t connect their bank accounts to your app. Using APIs to connect with banks and other financial institutions ensures seamless transactions, keeping your users happy and engaged.

Rapid Technological Changes: Does it feel like the tech world changes faster than you can keep up? Join the club! But remember, continual learning and adaptation are the keys to success. Staying abreast of industry trends and technological advancements will help you stay ahead of the curve.

So, while developing a P2P payment app might seem like climbing Mount Everest, with the right strategies in place, you’ll be standing on the summit in no time. As you know, every challenge is an opportunity in disguise.

Regulatory Updates: Navigating the Legal Landscape of P2P Payment Apps

Keeping up with the ever-evolving legal landscape of peer-to-peer (P2P) payment apps can feel like trying to hit a moving target. But don’t let that deter you. Staying informed about regulatory changes is crucial, not only for compliance but also for gaining a competitive edge. Let’s dive into some recent updates that could have significant implications for your app.

-

Consumer Financial Protection Bureau (CFPB): The CFPB recently proposed new rules to increase transparency in the P2P payments market. These changes aim to provide consumers with more information about fees, exchange rates, and access to funds. Transparency is no longer just good practice—it’s becoming a legal requirement.

-

Financial Crimes Enforcement Network (FinCEN): FinCEN’s updated guidelines now require P2P payment apps to comply with the Bank Secrecy Act. This means implementing robust anti-money laundering (AML) and know-your-customer (KYC) protocols. Compliance is non-negotiable, so make sure your app is up to the task.

-

Federal Trade Commission (FTC): The FTC has been cracking down on deceptive or misleading practices in the P2P payments industry. It’s essential to ensure that your marketing materials and user agreements are clear, truthful, and not misleading.

-

European Union’s Revised Payment Services Directive (PSD2): While this regulation directly applies to European companies, it’s setting a global standard for secure customer authentication and open banking. Even if your app is primarily targeting the US market, keeping an eye on international regulations can give you a heads-up on potential future changes at home.

-

California Consumer Privacy Act (CCPA): California’s groundbreaking privacy law has set a new standard for data protection. Given its influence, it’s worth considering how similar regulations might spread to other states or even federally.

Regulations can seem daunting, but they’re also an opportunity. By staying informed and proactive, you can turn regulatory compliance into a competitive advantage. After all, in the world of P2P payments, trust is currency—and nothing builds trust like demonstrating your commitment to legal compliance and consumer protection.

Cost of Developing a P2P Payment App

Please note that we do not do fixed-price projects. So please consider the price points here as high-level approximations. To keep it short, the approximate cost to build custom money transfer software is around $80K-120K for an MVP and $200K-$300K for a feature-rich p2p payment app.

To provide additional clarity: the MVP scenario allows you to obtain an initial releasable version that can be tested by your most loyal customers and users for feedback and iterative improvements.

On the other hand, the more advanced scenario involves releasing a public version that is fully prepared to handle spikes in usage and automates the process of gathering customer feedback.

Related: App Development Costs: How to budget for your application

Topflight’s Experience with p2p Payment Apps

At Topflight, our venture into the realm of P2P payment solutions has been through our exciting collaboration with Coronation Group on their wealth management and investing app ‘Wealth by Coronation’, which incorporates several p2p payment features.

In a bold effort to democratize Nigeria’s retail investment and personal finance management markets, Coronation Group partnered with Topflight to develop a robust yet intuitive investment and wealth management app. Named ‘Wealth by Coronation’, this app is a testament to the power of technology in unlocking financial services for non-professional investors.

The ‘Wealth by Coronation’ app stands out in Nigeria’s booming fintech market, offering a premium experience to its retail customers. It’s as user-friendly as Robinhood but offers a broader range of wealth management options. The app includes features like:

The ‘Wealth by Coronation’ app stands out in Nigeria’s booming fintech market, offering a premium experience to its retail customers. It’s as user-friendly as Robinhood but offers a broader range of wealth management options. The app includes features like:

- Personalized concierge service

- Watchlist and recommendations

- Take-profit and stop-loss trading

- Price charts and price alerts

- A built-in mobile wallet

Beyond investments, the app provides a comprehensive view of a customer’s entire wealth management plan. Users can access wealth advisors, set financial goals, track balances and transactions, manage personal trusts and wills, and make payments. Notably, it has P2P payment features like topping up balance and making payments, setting a golden standard for financial independence and sustainable wealth creation.

The app was built on a tech stack that includes React Native, Serverless Node.js, Verify.Me, Woven Wallet, Paystack, and AWS. This allowed for a quick launch on both iOS and Android platforms while staying within budget.

For more details on how Topflight and Coronation Group achieved this feat, read the full case study here.

How Topflight Can Help

Some the most exciting fintech products we built at Topflight include:

- a wealth management app (investing, insurance, etc.) for a bank

- a crypto savings account (read the case study)

- a smart-budgeting app (read the case study)

- metaverse defi apps, including a DEX and NFT marketplace (read the case study)

And even though these applications don’t focus on pure P2P payment experience, most of them include relevant use cases. We’ll be happy to help you innovate the p2p space, especially if you’re looking to develop a p2p application that unites fiat and crypto ecosystems.

Hopefully, you found answers to some of your questions about how to make a money transfer app in this blog. If you’d like to discuss your fintech idea and the mobile payment application development process in detail, please schedule a call with our experts.

Related Articles:

- How to make a blockchain payment system

- How to Create a Loan App

- How to Develop a Crypto Trading App

- How to Build a Crypto Exchange

- How to Build a Budget App

- Cost to Start a Crypto Exchange

[This blog was originally published in December 2021, and has been updated for more recent content]

FAQ

How long does it take to build a P2P payment app?

4 to 6 months for an MVP version.

Can I use cross-platform apps like Flutter and React Native?

Yes, some of the bigger names on the market use these technologies to optimize their development budgets.

How to build a payment app to send and receive money in cryptocurrencies?

You will need to create a crypto wallet and solve the issue of storing contacts and their blockchain addresses conveniently.

Are there any regulatory fintech sandboxes in the US for piloting a mobile transfer app like they have under Financial Conduct Authority in the UK?

Unfortunately not. Therefore, you will need a strong partnership with a traditional financial institution that’s ready to try new things.

How much does it cost to make an app like Cash App?

$300,000 — $500,000.

What are some of the most popular features in p2p payment apps?

Transferring money by specifying an email address, an option to request money, notifications upon detected fraudulent activity, paying bill payments through an installment plan, etc.

How do you set up a p2p payment account?

Setting up a P2P payment account is typically a straightforward process. Step 1: Download the P2P payment app from your device’s app store. Step 2: Open the app and select the option to create a new account. Step 3: Provide the requested information, which usually includes your name, email address, and phone number. Step 4: Verify your account, often through a code sent to your email or phone. Step 5: Link your account to your bank account, credit card, or debit card by providing the necessary details. This allows for the transfer of funds. Step 6: Set up security measures such as a password, biometric authentication, or two-factor authentication to protect your account.

Are there any ready-made solutions that I can use to spearhead p2p payment app development?

Yes, but I cannot recommend a single one without our team verifying the solution against your product vision